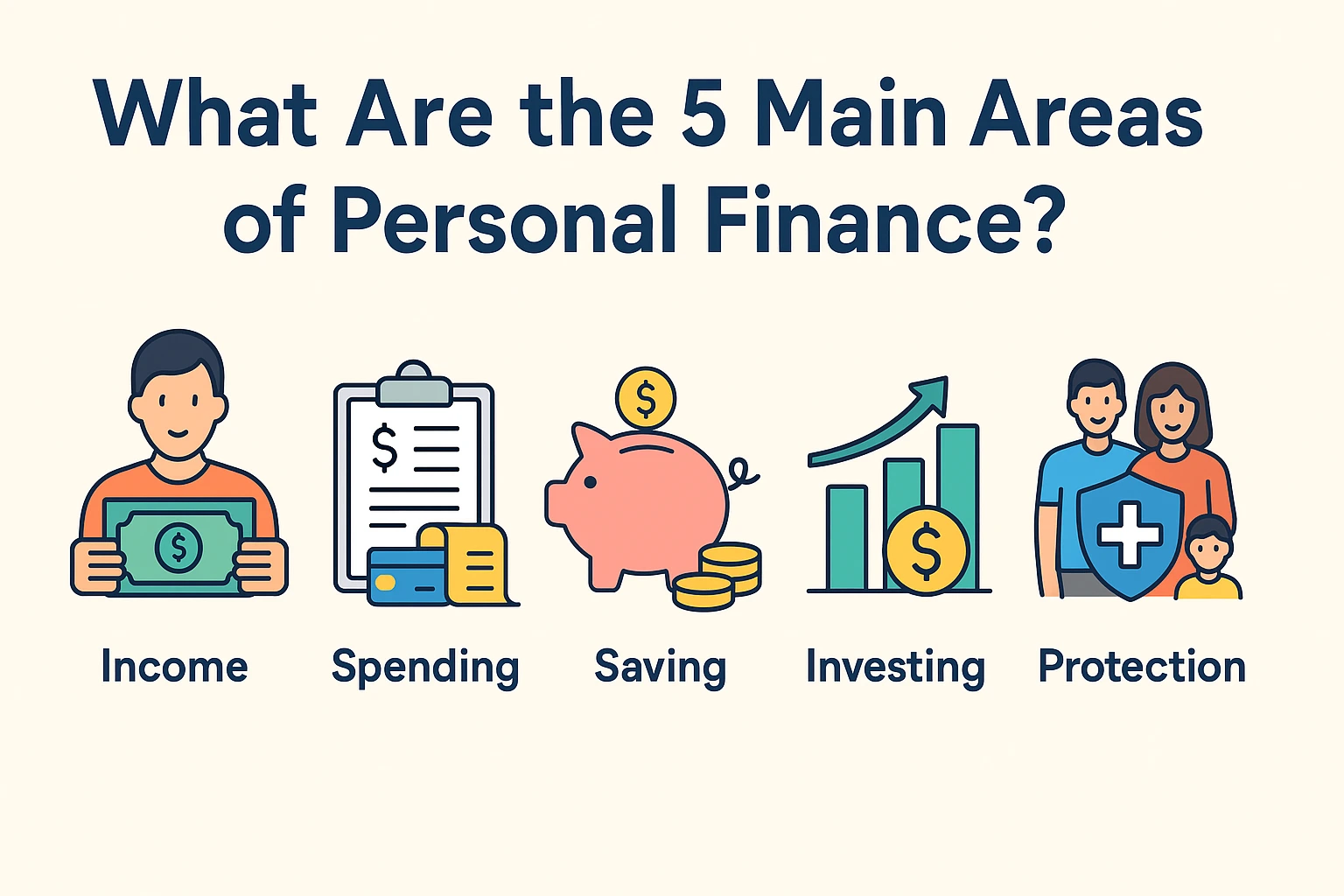

Money touches every part of life. We earn it, spend it, and save it. When you learn how to handle money, you gain freedom and control. Personal finance is the plan you make to reach that control. Experts group it into five main areas. Each area works with the others. Together they guide how you earn, spend, and grow your money.

This guide explains the 5 main areas of personal finance in plain words. You will see how each part fits into daily life and why balance matters.

Table of Contents

1. Income

Income is the money you bring in. It can come from a job, a small business, or side work. Some people also earn from rent, dividends, or interest. Your income sets the base for all other money plans. You cannot save or invest if you have no cash flow.

Start by knowing your total monthly income. Write down every source, even small ones. This shows what you have to work with. Next, track how steady each source is. A fixed salary is more stable than sales that change each week. Stable income helps you plan ahead with less stress.

Growing income can be as key as cutting costs. Skills, education, and smart career moves can raise your pay. A side hustle, like tutoring or freelance work, adds extra. More income gives you room to save, invest, and handle surprises.

2. Spending

Spending covers every bill and purchase. Rent, food, transport, clothes, fun, and debt payments all count. Knowing where each dollar goes helps you avoid waste.

Start with a simple budget. List needs like housing, food, and power. Then add wants such as eating out or streaming. A common guide is the 50-30-20 rule: 50 percent for needs, 30 for wants, 20 for savings and debt. Adjust it to fit your life.

Watch for small leaks. Daily coffee or unused subscriptions can add up. Review your bank and card statements each month. Cancel what you do not use. Pick cheaper options when quality is the same. A budget is not a cage. It is a tool that shows where your money flows and lets you choose.

3. Saving

Saving is money you set aside for the future. It protects you from shocks like job loss or a car repair. It also helps you reach goals such as a home, college, or travel.

Start with an emergency fund. Aim for three to six months of living costs. Keep it in a bank account that you can reach fast. This is your safety net. It keeps you from using high-interest credit in a crisis.

After the emergency fund, save for short-term goals. These might be a vacation, a car, or a wedding. Use separate accounts if it helps you stay on track. Automatic transfers right after payday make saving easy. Treat savings like a fixed bill you must pay.

Consistency matters more than size at first. Even small amounts grow with time and steady effort.

4. Investing

Investing means putting money into assets that can grow. Stocks, bonds, mutual funds, real estate, and retirement accounts are common options. The goal is to build wealth over years.

Investing carries risk, but smart steps can reduce it. Start by learning the basics. Stocks can rise and fall fast. Bonds are steadier but grow slower. A mix of assets spreads risk. Many people use index funds for broad market exposure at low cost.

Time in the market matters more than timing it. Regular contributions, even small ones, build wealth. Compound growth works best when you start early. Reinvest dividends and stay the course during market swings.

Match investments to your goals and risk comfort. Money for retirement can handle more risk than cash you need in two years. Review your plan once or twice a year and adjust as life changes.

5. Protection

Protection guards what you have. Insurance and planning keep a sudden loss from wiping out years of work. Health, life, auto, home, and disability insurance all play a role.

Health insurance is vital. A single hospital stay can drain savings. Life insurance protects loved ones if you die early. Disability insurance replaces income if you cannot work. Home or renter coverage shields property. Review each policy to be sure limits fit your needs.

Protection also includes legal planning. A simple will, power of attorney, and named beneficiaries help your family if you cannot act. These steps spare them stress and cost.

Do not see insurance as wasted money. It is a shield that lets you take other risks with confidence.

How the Five Areas Work Together

Each area links with the others. Higher income lets you save and invest more. Good spending habits free cash for savings. Solid savings let you invest without fear. Strong protection keeps you on track when trouble comes.

Think of personal finance as a house. Income is the foundation. Spending is the frame. Saving and investing build the walls and roof. Protection is the lock on the door. Weakness in one part can hurt the whole structure.

Steps to Improve Your Personal Finance Plan

- Check your income. List every source. Look for ways to grow it.

- Create a budget. Track all spending for a month. Spot waste.

- Build an emergency fund. Save at least three months of expenses.

- Start investing early. Use simple, low-cost funds if new to it.

- Review insurance. Make sure health, life, and property coverage fit.

Small changes make a big difference over time. Set clear goals. Automate where possible. Review your plan each year.

Final Thoughts

The 5 main areas of personal finance—income, spending, saving, investing, and protection—cover every part of money life. You do not need to be a math expert to master them. You need a plan and steady action.

Track income, spend with purpose, save first, invest for growth, and protect what you build. Focus on progress, not perfection. Each smart step brings you closer to freedom and peace of mind.

Frequently Asked Questions For 5 main areas of personal finance

Q1.What are the 5 main areas of personal finance?

Income, spending, saving, investing, and protection.

Q2.Why is saving important in personal finance?

It protects from emergencies and helps reach goals like home or travel.

Q3.How does investing differ from saving?

Saving keeps money safe for short-term use; investing grows money over time.

Q4.What is the role of protection in personal finance?

Insurance and legal planning safeguard income, health, and assets from risk.